Inflation linked bonds: Why we have upped our exposure following the US election

- 23 November 2020 (7 min read)

The extraordinary monetary and fiscal support from central banks in the wake of the coronavirus pandemic has been welcome news for investors. More recently, the positive news on the development of the first effective coronavirus vaccines has spurred demand for riskier assets, as an end in sight to the pandemic should support an accelerated economic recovery.

Such bullish macroeconomic events have historically attracted demand for inflation-linked bonds. At the same time, in our view, the structural transformation we are seeing across global economies is helping to underpin the asset class – meaning that even before news of a vaccine, many investors have been considering these as part of a fixed income portfolio.

Inflation-linked bonds have performed well so far in 2020 - and we expect them to continue to be potentially attractive to investors, primarily as a result of four main drivers.

2020 – Inflation-linked bonds returns

| Return (hedged in euros) | |

| US Treasury Inflation-Protected Securities (TIPS) | 7.41% |

| UK inflation-linked bonds | 4.80% |

| Euro inflation-linked bonds | 1.27% |

| Canadian inflation-linked bonds | 9.88% |

| Australian Commonwealth inflation-linked government bonds | 3.35% |

| New Zealand inflation-linked government bonds | 12.1% |

Source: Bloomberg Barclays Indices, as of 31 October 2020

Inflation expectations remain depressed

Inflation is expected to remain low for the rest of this year, and pick up again in 2021. Global lockdowns and the resulting fall in economic activity had a clear effect on prices for a variety of reasons, but we are already starting to see signs of higher pricing in some sectors, such as food, medical care services, and used vehicles1 .

This could suggest that market expectations are too low. Indeed, short-term inflation swaps are indicating that market pricing is more pessimistic than economists' forecasts that inflation will rebound next year. While this may only look like a near-term story, inflation expectations are generally well correlated with short-term realised inflation developments.

This suggests to us that when inflation will pick up in 2021 this may give a boost to so-called inflation breakevens i.e. the difference between a nominal bond’s yield and that of an inflation-linked bond of the same maturity.

Loose fiscal policy vs. economic decline

Mature economies are facing the deepest economic contraction since the 1929 crisis. But the environment of loose fiscal policy should continue to provide a buffer against economic contraction. Governments have been quick to respond to the shock in a globally-coordinated fashion through monetary and fiscal policy, and with provisions such as furlough schemes, lending and guarantees being extended.

This should help strengthen the economic recovery. And unlike the years following the 2008/2009 financial crisis, we believe that early fiscal austerity is unlikely, as even the International Monetary Fund is pleading for more public spending2 . We therefore believe that inflation will recover in 2021, both at a headline and core level – but we do not expect a dramatic rise.

For example, furlough schemes are complementary rather than stimulatory, replacing lost wages. Headline inflation is likely to remain underpinned by oil prices, which we expect to be solid in 2021 after slumping this year as the pandemic spread. We anticipate headline inflation rising to between 1.5% and 2% in the Eurozone and 2.5% and 3% in the US by mid-2021.

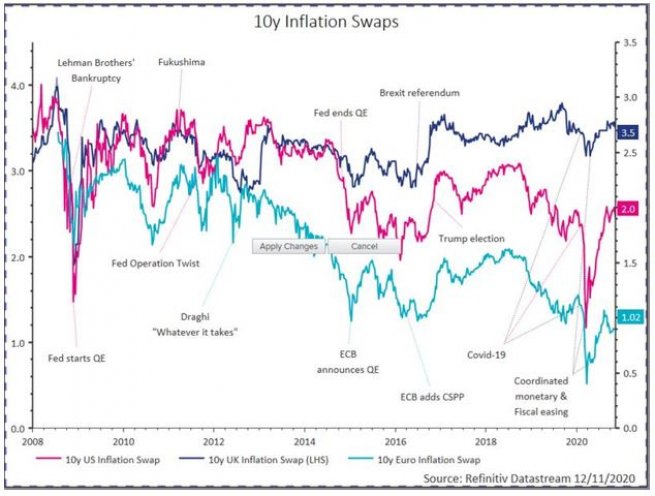

Core inflation rates, which do not include oil prices, are also expected to rebound from current levels from the second quarter of 2021, climbing towards 2% in the US and 1% in the Eurozone. The chart below shows how fiscal and monetary policies can lift inflation expectations.

- VVMgQ29uc3VtZXIgUHJpY2UgSW5kZXgsIE9jdG9iZXIgMjAyMCwgVVMgRGVwYXJ0bWVudCBvZiBMYWJvcg==

- aHR0cHM6Ly93d3cuZnQuY29tL2NvbnRlbnQvNzIyZWY5YzAtMzZmNi00MTE5LWEwMGItMDZkMzNmY2VkNzhm

Monetary policy is targeting economic growth

Central banks’ monetary policies are focusing less on fighting inflation and more on driving economic expansion.

As budget deficits reach historical highs (excluding during wartimes), we believe that central banks will need to maintain easy monetary policy for the foreseeable future.

Indeed, some major central banks are undertaking strategy reviews, which are seeing policymakers’ focus gradually shifting from fighting inflation towards supporting economic output or the job market on top of avoiding deflation.

Historically, inflation-linked bonds have generally been well supported when non-conventional monetary policy is being implemented, as the table below shows. As we are facing some years of innovative and unconventional monetary policy, we expect real interest rates to continue to decrease over the course of 2021.

| Date | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

| US monetary policy stance | Easing | Easing | Tightening | Tightening | On hold | On hold |

| ICE BofA 1-5 Year Global Inflation-Linked Government Index | 1.3 | 1.5 | -1.6 | -0.4 | 1.8 | -0.3 |

| ICE BofA Global Inflation-Linked Government Index | 6.7 | 5.4 | -2.6 | 1.3 | 8.6 | -0.9 |

| Date | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

| US monetary policy stance | On hold | Normalisation | Easing | Easing | Easing | Easing |

| ICE BofA 1-5 Year Global Inflation-Linked Government Index | -0.5 | -0.9 | 3.6 | 4.4 | 3.7 | 9.1 |

| ICE BofA Global Inflation-Linked Government Index | 9.5 | -5.0 | 7.0 | 11.8 | 5.0 | 8.6 |

Returns are euro-hedged. Source: ICE BoAML indices, as of 31 October 2020

Long-term risks to inflation are on the rise

Globalisation has been the main source of global disinflation. While we do not expect it to go away in the near term, the prospects for more nationalist policies and trade disputes such as Brexit or the US/China trade war may put a brake on the import of cheap goods creating a risk of a higher trend in inflation.

Fiscal dominance is the other medium-term risk that is raising the attractiveness of inflation-linked bonds. As central banks have been increasingly supporting fiscal spending, we would venture that they have gradually lost their independence.

There is a chance that they would eventually need to decide between rising rates in the event of an inflation shock or tolerating it because higher rates would derail the debt sustainability. This is probably one of the reasons why long-term inflation breakevens have outperformed shorter maturities since March 2020, when those measures have been announced, as shown in the table below.

| Year-to-date US inflation breakeven performance | |

| Less than one year | 0.49% |

| One to three years | -0.37% |

| Three to five years | -0.16% |

| Five to seven years | 0.07% |

| Seven to 10 years | 0.29% |

| 10 to 15 years | 3.98% |

| 15 years+ | 4.15% |

Source: AXA IM, based on ICE BoAML indices, as of 31 October 2020.

How we are positioned

Despite Joe Biden’s victory in the US Presidential election, the lack of a significant “blue wave” of votes means, we believe, less likelihood of fiscal support - and more monetary support that will be needed. This removes the downside risk for inflation-linked bonds of sharply higher real yields. We expect yields to remain lower for even longer.

As a result, we have added five-year US Treasury Inflation-Protected Securities (TIPS) to our strategies, and where possible have been going long inflation breakevens. Buying long real yields is a strategic trade for 2021; leveraging on easy monetary policies and essentially focusing on the five-year sector on the curve, which we believe can potentially provide a good trade-off between inflation and duration.

Our position in long inflation breakevens is more tactical but we expect that this type of instrument will do well in the first half of 2021, as headline inflation numbers rebound.

The last decade suggests that easy monetary conditions by themselves do not necessarily create inflation. However, the current combination of extreme fiscal and monetary policies coupled with structural transformations in the global economy is underpinning inflation expectations – and drawing investors back into inflation-linked bonds.

We expect this trend to continue during the first half of 2021 and believe this is an area that can potentially offer attractive returns, particularly at the front end of the curve.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Disclaimer

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, AXA IM HK, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2023 AXA Investment Managers. All rights reserved.