Multi-Asset Investments Views: Bad news on the way… and therein lies the good news

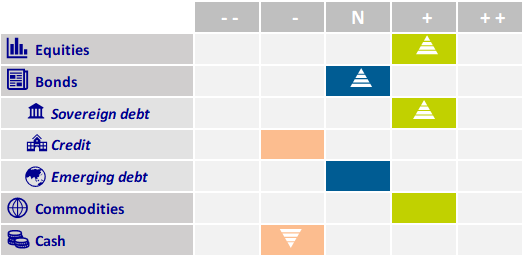

Our positioning

- Positive on global equities – In the context of a macroeconomic soft landing combined with strong microeconomic fundamentals, we expect further upside in developed market equities.

- Neutral on duration – The past two months provided the technical consolidation in rates we were looking for, after what we deemed as a too fast and too strong end-2023 rally. Building a higher duration position starting from current levels makes sense for our multi-asset strategies.

- Positive on US dollar, e.g. against GBP – We maintain our exposure to the US dollar with economic surprises most positive there. Conversely, we see idiosyncratic factors in the UK weighing on GBP.

Our views

The markets have digested an uncomfortable amount of outlook volatility over the past three months, from the soft-landing consensus that supports all asset classes to an emerging narrative, marginally for some and materially for others, of the possibility of a no-landing. This latter scenario would translate into a higher required level of neutrality for monetary policy in the US.

At the other end of the spectrum, there are even die-hard advocates of recession still out there despite US GDP growth repeatedly printing above potential. Since October, short-end interest rates have priced then de-priced from three to near seven, and then back to three Federal Reserve (Fed) rate cuts in the twelve months ahead. Meanwhile, actual volatility measures in the fixed income market have been well-behaved relative to last year’s ructions. Along with the artificial intelligence profitability and productivity story, risk assets and equities especially have held up very well in the face of higher bond yields, or indeed performed strongly. Supply year-to-date was particularly heavy in fixed income space, yet investors’ demand absorbed it with barely a ripple.

The elements that could still drive a slowdown in the US, or even a tip into recession in Europe, have however not disappeared. They are merely lagging the news-flow elsewhere. Our Macroeconomic Research team sees some weakness ahead, as the positive drivers of US activity last year struggle to reassert themselves in 2024. And it is this weakness, eventually to be evidenced in the labour market and wages, that will allow the Fed to engage with policy normalisation this year.

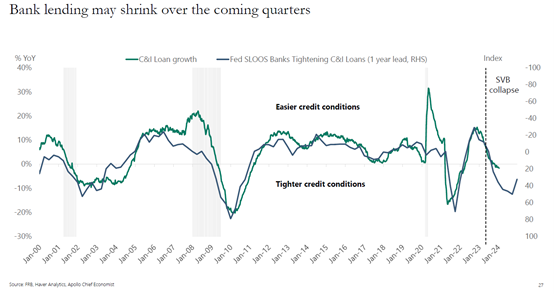

Demand in the US last year was initially driven by excess savings on household balance sheets, secondly by positive real wages, and thirdly by US fiscal spending that took the budget deficit up towards 10%. These conditions are unlikely to be repeated. Main Street is not as healthy as Wall Street and indices of financial conditions are strongly divergent between the two. The depth of damage from commercial real estate on small and mid-size bank balance sheets remains a source of concern at this stage in the cycle. Not so much as a systemic risk, but rather as a hurdle to their ability to extend credit. Add to this an apparent lack of enthusiasm from Chinese authorities to counter demand deflation in the world’s second largest economy and markets may well require some policy support to maintain the very positive start to the year.

Should the recent inflation and jobs prints prove to be bumps rather than U-turns, and the pace of disinflation holds with the past six months trends, then the weaker news from Main Street should focus the Fed’s attention on the path to a series of cuts that will bolster the outlook for the US and allow the European Central Bank to follow suit with rate cuts.

Fast money positioning has been reduced on rates whilst institutional investor demand is proving resilient in the face of heavy supply. This argues for building a stronger duration position at current levels for our multi-asset strategies. The path to lower rates will become clearer should the bad news on Main Street persist in the next couple of months. Whilst supporting our duration call, further softening of financial conditions will also provide support to equities where valuations are currently at lofty, albeit not extreme levels.

Divergence in financial conditions between Wall Street and Main Street

Source: FRB, Citi, Bloomberg and AXA IM

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.