Metaverse Mythbusters

Key points:

- The Metaverse is already a new and exciting source of opportunities, with unprecedented potential for scale

- The pace of technological advances has accelerated over the past 50 years, allowing credible opportunities to become investible far earlier

- We aim to clarify some of the most common questions or misconceptions that investors may have

The Metaverse has created a significant amount of buzz in the investment sphere as well as the technology industry and wider media, and with good reason. With a projected global market size of over $800bn by 2030

Isn’t the Metaverse a relatively new phenomenon?

The Metaverse is exciting source of opportunities due to its ability to draw upon the advances in technological capabilities across hardware, software and infrastructure that, after several decades of development, now move at a far faster pace. There had previously been four key computing platforms introduced over the past 50 years

How do you find meaningful opportunities amongst the hype, and mitigate the risk of early adoption?

The respected business analysis firm Gartner publishes a ‘Hype Cycle’ for innovative, emerging technologies which are expected to disrupt the existing markets. The Metaverse has made multiple appearances on this annually published chart under various guises such as augmented reality (AR) and virtual reality (VR) which were languishing at the bottom of expectations in 2017. For 2022, the Metaverse collectively appears strongly back in the ‘rising expectations’ segment of the chart and is not expected to plateau for more than ten years (which suggests a promisingly tong-term growth horizon)

‘The Metaverse’ sounds niche compared to traditional technology strategies, is there a sufficiently large investment universe for investors?

One of the key drivers of the Metaverse’s potential is the scope and scale that is possible. It’s true that its early origins sit within the gaming world, but now its capabilities are being recognised by major players in industry and in the workplace (see our previous articles on Metaverse Working, and Enablers). Another important point to consider is the concurrent rise of capabilities in artificial intelligence (AI), which exists synergistically alongside the Metaverse and allows it to grow at an even faster pace by utilising technologies that can work more rapidly and more efficiently than a human can.

Of course, one must also not underestimate the depth of opportunities in the core gaming and socialising themes of the Metaverse. Almost 40% of the world’s population are estimated to have played games in 2022 – a potential consumer base of three billion people cannot be dismissed.

OK, sounds promising, but how can this concept be adequately captured in an investment portfolio?

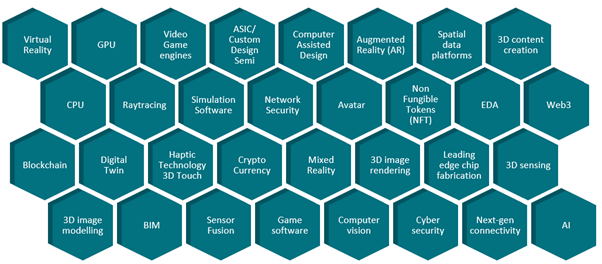

As suggested by the Gartner research, we are at the early innings of a significant transformation, which should gradually unleash its full potential in the next decade. This presents a huge opportunity to invest in the pioneering technology companies of today – many of those positioned at the leading edge of innovation. Investing in these companies offers exposure to a range of underlying technologies, which we characterise as the building blocks that underpin the development of the Metaverse. These blocks come together to form what we refer to as the ‘Metaverse Wall’. To paraphrase Gartner, it is our expectation that the Metaverse cannot be defined as a single technology, but a rather a combination of numerous individually important, discrete and independently evolving technologies that interact with one another to give rise to a mega trend – the Metaverse.

The Metaverse Wall:

Source: AXA IM for illustrative purposes only.

We want to participate in the growth of the Metaverse and all of its associated, promising opportunities in line with an investment philosophy, which favours quality growth companies. While the timeline for the Metaverse’s rise to prominence may be up for debate, a robust investment approach can aim to ensure focus on combining Metaverse relevance with solid fundamentals.

Companies shown are for illustrative purposes only as of 20/04/2023. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities.

Risks

No assurance can be given that our equity strategies will be successful. Investors can lose some or all of their capital invested. Our strategies are subject to risks including, but not limited to: equity; emerging markets; global investments; investments in small and micro capitalisation universe; investments in specific sectors or asset classes specific risks, liquidity risk, credit risk, counterparty risk, legal risk, valuation risk, operational risk and risks related to the underlying assets.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.