Multi-Asset Investments Views: Don't let me down

KEY POINTS

“When you see one cockroach, there are probably more”. This metaphor was coined by JPMorgan chief executive Jamie Dimon after the US regional bank Zions Bancorporation revealed it has been defrauded of around $60m through manipulated loan structures. The fear is that if multiple frauds surface in quick succession, it may indicate deeper systemic weaknesses, especially in some corners of the private credit markets. Recently, the bankruptcy of First Brands Group, a privately held US auto parts manufacturer with opaque off-balance sheet financing, and the collapse of Tricolor Holdings, a subprime auto lender accused of fraud, raised investors’ concerns about governance risks in more marginal parts of the financial system. This last episode of fraudulent activity briefly rattled credit markets and focused concerns on vulnerabilities in the private credit ecosystem.

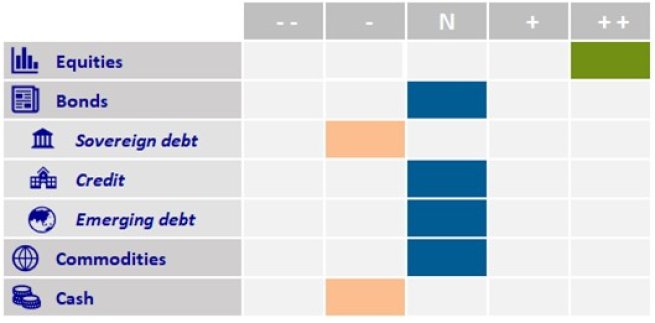

We remained invested but quiet tactically on credit markets and have been for some time, as we considered spreads to be too tight, offering an unattractive risk/reward profile, but we are not worried about an imminent credit crisis. At below 2%, the non-performing loans ratio of US banks remains far from levels seen in the aftermath of the global financial crisis (it peaked at 7.5% in 2010). The loose covenants and light regulatory environment in parts of the private credit market are not new and can be traced back to deregulatory trends that began during US President Donald Trump’s first term. We remain neutral on credit as we prefer to concentrate our risk-taking within equities.

After six months without a daily correction of more than 2% for the S&P 500, equities endured a bout of volatility on 10 October when Trump took to social media to berate a hostile trade attitude from China relating to its actions on rare earths and export controls. In a classic Trump gesture, he first threatened a massive increase in tariffs on Chinese products, only to finally appease markets later by confirming he will be meeting President Xi Jinping in South Korea - the first time since Trump returned to the White House. As tariff uncertainty made a comeback, the positioning reduction from volatility-controlled strategies and discretionary investors was well absorbed by the market judging by the limited losses on the S&P 500. This is especially important considering the return to a higher volatility regime also triggered some profit taking in high-momentum trades which have been retail favourites since the market rally began in late April.

In our view, the hyperbolic rise in the gold price and other precious metals is another expression of the speculative trend which was fueled by substantial inflows on exchange-traded funds from individual investors as well as price-insensitive demand from central banks, rather than a higher expression of defiance towards US Treasuries and the dollar. Being at its most overbought in 45 years, the gold sell-off reflects a positioning wipe-out rather than any macroeconomic shock.

We view the recent reduction in investor positioning as a constructive development. From a fundamental standpoint, the macro and micro backdrop remains supportive. Earnings continue to send a constructive message overall in both the US and Europe. The beat rate for the S&P 500 is higher than usual, above 80% at the time of writing and earnings-per-share is on track to exceed 10%, assuming the historical trend of estimate revisions. The combination of looser monetary policy in a non-recessionary economic environment, enthusiasm around artificial intelligence adoption, ongoing fiscal stimulus, and resilient corporate earnings creates a favourable setting for risk assets into year end.

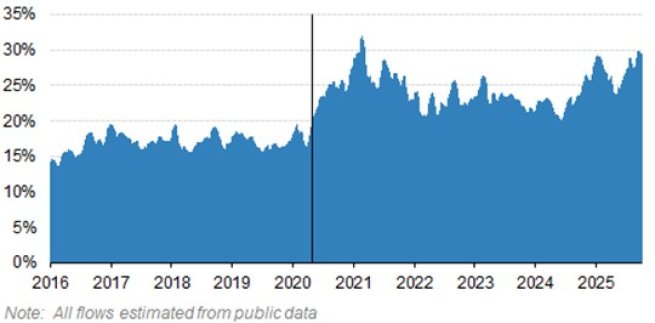

Retail investors’ participation has shifted higher since the pandemic, and has been the backbone for equity risk through the summer

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.