Five reasons why Europe is back on the investment map

KEY POINTS

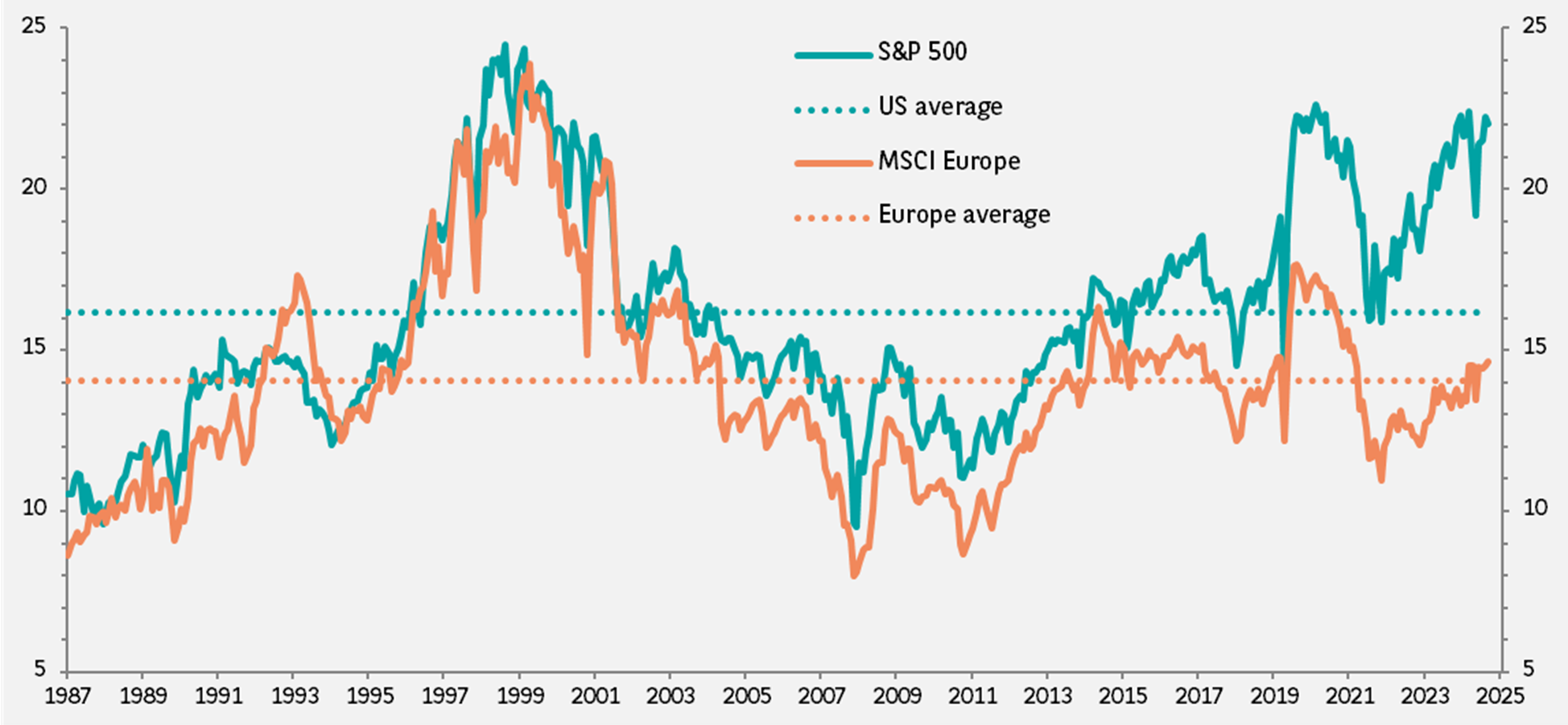

1.Attractive valuations

Attractive valuations are a powerful argument in favour of European equities, which currently trade at significant valuation discounts compared to the US.

The next-12-month price-earnings ratio for the MSCI Europe index is currently 14.6 times, slightly above the average since 1987 of 14 times. By contrast, in the US valuations are close to all-time highs, currently 22 times expected earnings.

Europe's average dividend yield is near 3.3% substantially exceeding the US average of about 1.3%.

Exhibit 1: Valuations far lower for European Equities

Next-twelve-month price-earning ratio

Data as at 26 August 2025. Sources: IBES, FactSet, BNP Paribas Asset Management

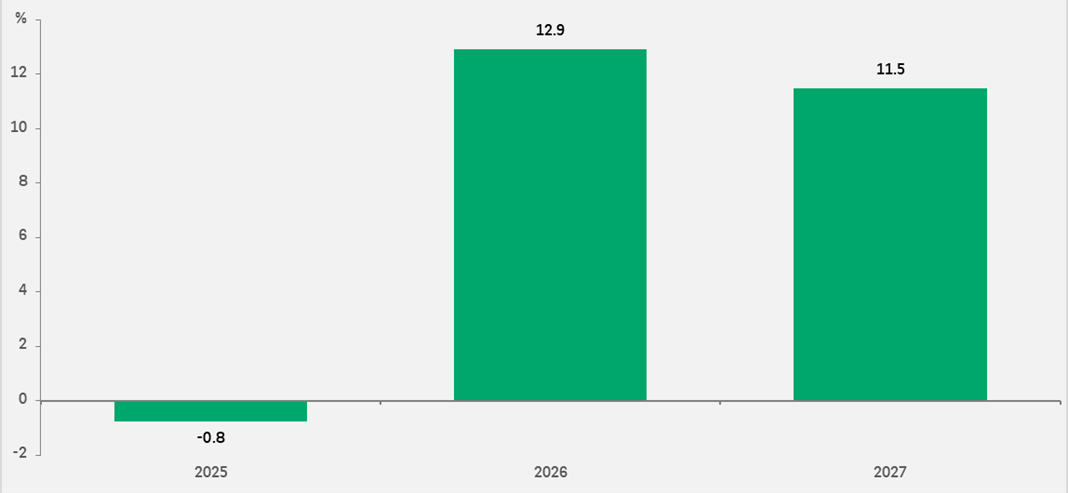

2.Recovery in earnings looking bright

Europe’s equity earnings outlook is brighter than it has been in many years. Consensus estimates for profit gains over the next couple of years see a big improvement on results compared to 2025, as Exhibit 2 shows.

The expected gains are particularly high in industries such as biotechnology, at 34% 2027/2026 earnings-per-share (EPS) growth, semiconductors (24%), and aerospace and defence (17%).

Exhibit 2: Earnings growth is expected to rebound sharply over the next couple of years

Year-on-year EPS growth

Data as at 26 August 2025. Sources: FactSet, BNP Paribas Asset Management

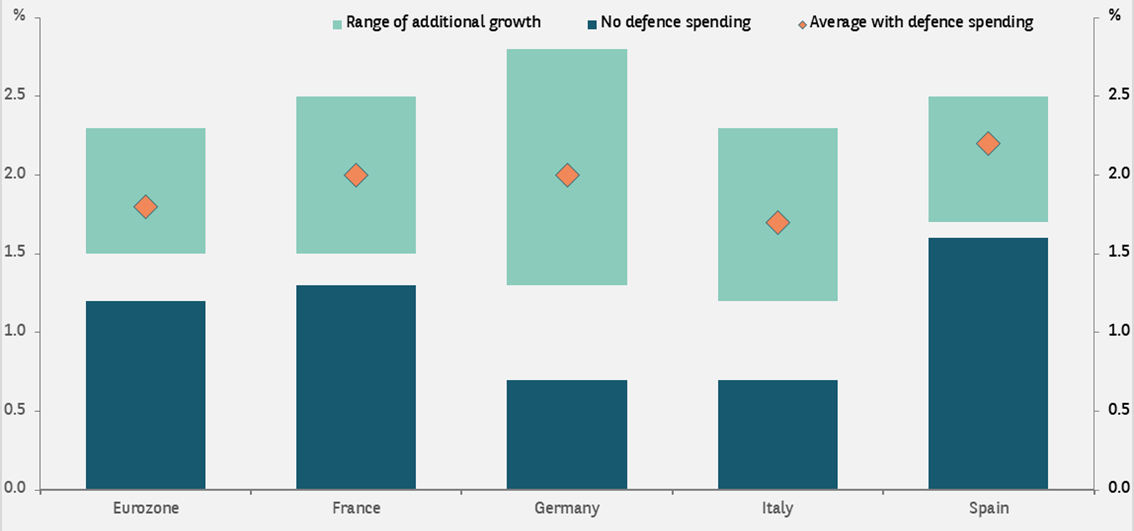

3.Unprecedented increase in Europe’s defence and infrastructure spending

US President Donald Trump’s push for greater defence burden sharing has borne fruit. There is broad acceptance across NATO countries to spend 5% of GDP on defence (broadly defined). We estimate the increase in defence spending could double the rate of real GDP growth across the region.

In addition, Germany has launched a major infrastructure and defence initiative, with investments of €500bn over the next 12 years in sectors including infrastructure, construction, renewable energy, healthcare and defence. This is a huge change for Germany and for Europe, which has historically been reluctant to spend to boost growth. This spending should have a meaningful impact on the continent’s growth rate as there is significant spare capacity in the economy.

Exhibit 3: GDP should increase across Europe

Real GDP growth

Data as at 26 August 2025. Sources: BNP Paribas Asset Management.

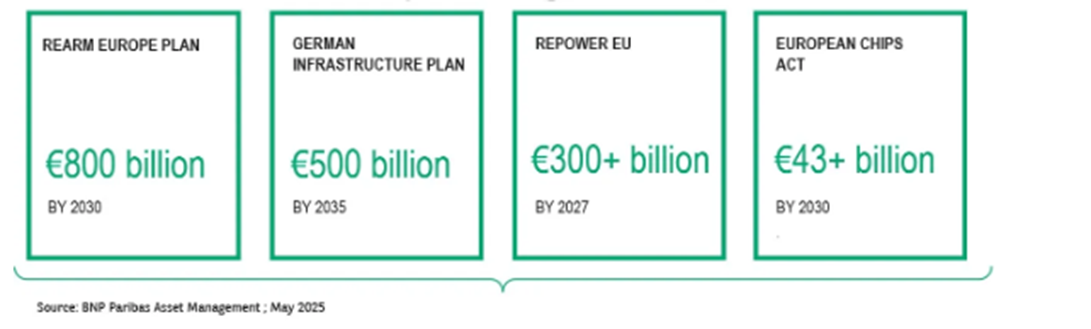

Europe’s pursuit for strategic autonomy has emerged as a central priority. For the region to act independently in key areas such as defence, energy, digital infrastructure and critical supply chains, investment plans for key public initiatives of a historic scale are in the pipeline.

The planned investments in Europe’s strategic autonomy amount to over €1.6trn

4.European fixed income offers opportunities

A crucial argument in favour of European fixed income is the confidence in the European Central Bank (ECB) to remain vigilant about inflation risk. Bondholders can rely on the ECB to protect them from inflationary pressures.

European fixed income, and in particular corporate debt continues to perform well with a relatively low level of volatility. In the first half of 2025 it has once again shown resilience in the face of considerable uncertainty.

European economic growth has been resilient in the first half of 2025. There is scope for a further pick-up in corporate investments and M&A activities as the Eurozone economy gains momentum in over the next 12 months. Companies in the corporate debt universe continue to prioritise deleveraging. Inflows into mutual funds and demand for collateral for Collateralized Loan Obligations are bolstering demand.

Our analysis shows fundamental characteristics of companies in the euro high-yield sector as relatively solid. Corporate results for the region continue to demonstrate the resilience of business models. Profit margins are stable, costs are well under control and there is potential for cash generation and balance sheet improvement. While there is limited scope for further significant spread tightening in 2025, we expect carry and security selection to drive performance.

5.Capital meets opportunity for private assets

In addition, private capital is positioned to help reshape the European continent’s global competitiveness by driving innovation, creating European champions, and mobilising the sizeable investments required. We believe Europe is emerging as one of the most compelling destinations for private asset investments.

The case for Europe factors in a gap in market valuation between European companies and their US-listed peers and falling financing costs. But it is primarily based on a growing conviction that economic reforms, combined with a stable environment for long-term investments, pave the way for major opportunities across Europe for all investors.

Europe offers macroeconomic and policy stability - combined with a highly investable structural roadmap. Public plans are creating tangible project pipelines and co-investment frameworks - not just wish-lists. Private capital is explicitly sought after to complement and scale up public capital across asset classes. Deployment is aligned with long-term objectives: impact, resilience, energy security, and re-industrialisation.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.