Take Two: Middle East conflict shakes markets; China cuts annual growth target

What do you need to know?

Global markets endured further volatility last week after the US and Israel took coordinated military action against Iran. Stocks fell sharply at the start of the week before then recovering some ground. Government bond yields rose also reflecting concerns over inflation, while oil prices increased on supply concerns. Over the week to Thursday’s close, the MSCI World NR Index fell 2% while the S&P 500 lost 1%, the Eurostoxx 600 fell 6% and Japan’s Nikkei fell 7%.* Market sentiment will likely remain largely driven by the scale and duration of the conflict.

*In US dollar terms. Source: FactSet, data as of 5 March 2026

Around the world

China cut its annual economic growth target to a range of 4.5%-5%, its lowest official goal since 1991, as it unveiled its new Five-Year Plan. The figure represents a decrease from its previous growth target of “around 5%”, which was met in 2025, as the country continues to face weak domestic consumption, property market challenges and global trade tensions. The draft Five-Year Plan, which will be put to a vote this week, also includes investments in innovation and technology, transport and energy, as well as further efforts to boost household spending.

Figure in focus: 1.9%

Eurozone annual inflation unexpectedly rose to 1.9% in February, the first time it has remained below the European Central Bank’s 2% target for two consecutive months since April 2021. The market had expected price increases to remain steady at 1.7%, to match January’s rate. Core inflation, excluding energy, food, alcohol and tobacco, increased to 2.4% from 2.2% in January. Separately, Eurozone GDP growth expanded by 0.2% in the fourth quarter, down from the previous estimate of 0.3% and Q3’s 0.3% growth. Elsewhere, the UK economy is now expected to expand by 1.1% this year, down from November’s prediction of 1.4%, according to new official forecasts.

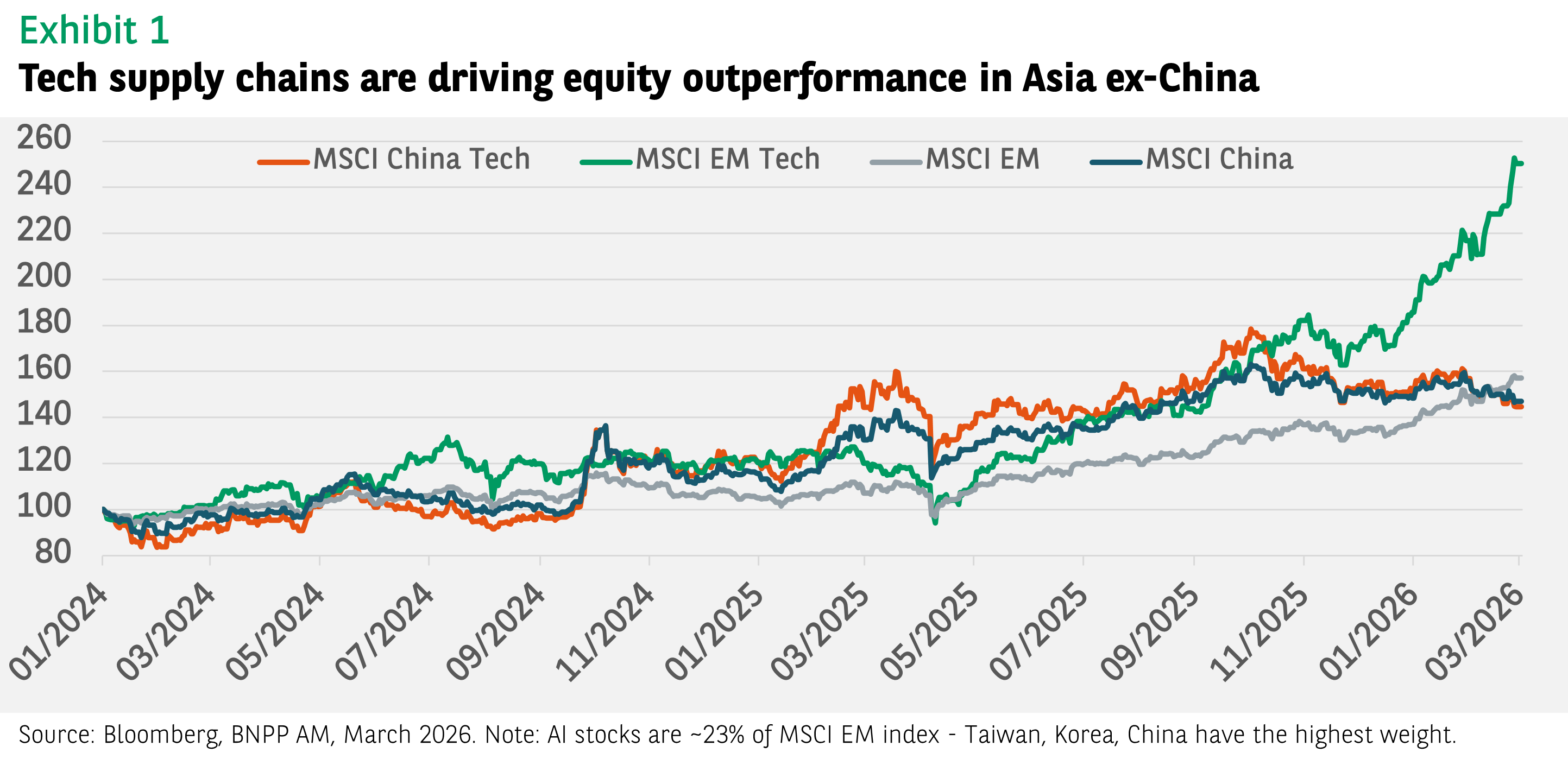

Chart of the week

The divergence between Asian markets, especially in the technology sector, highlights a dynamic shift in the regional landscape, driven by the global artificial intelligence capital expenditure boom. Hardware hubs in Asia-ex China, notably Taiwan and South Korea, are thriving due to increased demand for high-end semiconductors and advanced packaging. China’s tech sector, however, presents a more nuanced picture. While recent policy reforms and domestic AI innovations like DeepSeek have spurred some recovery, the sector still trails regional peers. China is actively working to establish its own technological leadership and independence, across software and hardware domains. Ongoing headwinds such as US export restrictions and regulatory uncertainty have kept investors on the sidelines.

Words of wisdom

EURO-3C: A €75m European Union project aiming to deliver “cutting-edge digital services” through telecommunication networks, cloud infrastructure and edge computing – which makes data processing faster. The European Commission unveiled the project, termed EURO-3C, at the Mobile World Congress last week. It said the initiative would reduce reliance on third-country providers, while bringing high-speed secure computing power closer to end-users. Involving a consortium of 87 companies and organisations, the project is intended to boost Europe’s digital and industrial competitiveness.

What’s coming up?

On Monday, China issues its latest inflation data while Tuesday sees a final estimate of Japan’s Q4 GDP growth published. The US reports February’s inflation rate on Wednesday - in January, US annual inflation fell to 2.4% from 2.7% in December. On Friday, Eurozone industrial production figures are published, while the UK posts monthly GDP data for January, and the US reports a second estimate of its Q4 GDP growth rate. The earlier estimate showed US GDP growth slowed to 1.4% in Q4 from Q3’s 4.4% growth.

Read more insights at the Investment Institute

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.