Take Two: OECD cuts global growth forecast; markets remain volatile

What do you need to know?

The Middle East conflict has dampened global economic growth expectations and lifted inflation forecasts, according to the latest Organisation for Economic Co-operation and Development outlook. The organisation revised down its 2027 global growth forecast to 3.0% from 3.1% but left its 2026 forecast unchanged at 2.9%. Inflation in the G20 advanced economies is now projected to be 4.0% this year, 1.2 percentage points higher than previously expected. The OECD warned however that a prolonged disruption to the oil market “could lead to significantly worse outcomes”. Global markets continued to endure further volatility last week with the MSCI World NR Index falling 1.5% over the week to Thursday’s close*.

*In US dollar terms. Source: FactSet, data as of 26 March 2026

Around the world

In the wake of the challenging geopolitical backdrop, business activity slowed in several major economies in March, the latest Purchasing Managers’ Indices showed. In the US, the provisional reading for the S&P Global composite activity index fell to an 11-month low, to 51.4 down from 51.9 in February, but remained in positive territory as a reading above 50 indicates expansion. Businesses reported a slightly weaker upturn in new orders and higher prices following the outbreak of the Iran conflict. The composite Eurozone PMI fell to 50.5, from 51.9, a 10-month low. Meanwhile the UK flash PMI slowed to 51.0 from 53.7, a six-month low.

Figure in focus: 1.3%

Japan’s annual inflation slowed to 1.3% in February, its lowest rate since March 2022 and down from January’s 1.5%. The lower-than-expected headline rate was largely driven by stabilising food prices and renewed electricity and gas subsidies. Core inflation, which excludes fresh food, fell to 1.6% from 2% while the closely watched ‘core-core’ inflation measure, stripping out fresh food and energy, eased to 2.5% from 2.6%. Separately, Japan’s business activity slowed in March as its composite PMI decreased to 52.5 from 53.9 a month earlier.

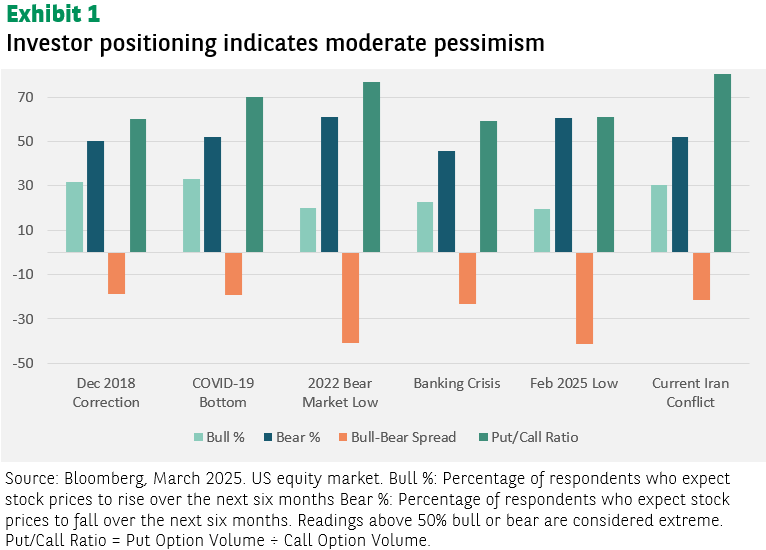

Chart of the week

Current investor positioning reveals a market caught between rebound expectations and caution. The relatively less pessimistic sentiment, along with elevated hedging activity, suggests investors are positioned protectively, in expectation for sentiment to gradually normalise. This cautious positioning could provide fuel for a market rally, based on possible catalysts for a de-escalation of the Middle East conflict, as heavily hedged markets often experience sharp gains when fear subsides, and protective positions are unwound. Short-term volatility could eventually give way to a rebound, as the market re-centres around the fundamental growth picture, which for now has not been altered.

Words of wisdom

Zettajoule: A zettajoule is a unit of measurement used for extremely large amounts of energy. Where one joule describes the amount of energy transferred when one watt of power is used for one second, a zettajoule is equal to a billion trillion joules – a number with 21 zeros. The rate of ocean warming was around 11.0-12.2 zettajoules over the past two decades, more than twice the rate seen between 1960 and 2005, according to a new report by the World Meteorological Organization. Along with other indicators, this suggests that Earth’s climate is more out of balance than at any time in observed history, it said.

What's coming up?

Monday sees the Bank of Japan issue its Summary of Opinions from its latest monetary policy meeting. On Tuesday a final estimate of UK fourth quarter GDP growth, and a flash estimate of Eurozone inflation for March, are published. The bloc issues its latest unemployment rate on Wednesday. On Friday, final PMIs are published for Japan, China and the US while the US also issues jobs data.

Read more insights at the Investment Institute

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.