US High Yield Market commentary and Outlook

US High Yield Trading Comments

(stats as of 8/31/23)

- Given recent rate volatility and general increase of US Treasury yields, high yield corporates have adjusted extremely well and remain close to year-to-date tights on spread and yield (385bps option-adjusted spread and 8.47% yield-to-worst). Defaults remain historically low and high yield companies still have plenty of runway to address near term financing needs.

- After being down as much as -1.18% through to August 21st, a +1.45% rally over the past 8 sessions has raised month-to-date high yield total returns to +0.29%. High yield is now up +7.22% year to date.

- Compression has remained the dominant theme for much of 2023 and continued in August with CCCs rallying +1.02% vs BBs being down -0.04%. Both higher rates and higher absolute dollar price resulted in BB bonds being targeted by accounts as sale candidates to buy lower dollar, riskier paper.

- While new issuance has been light, the early forward calendar for September looks fairly robust with a mix of M&A and more traditional refinancings. Banks have largely cleared out any hung debt remaining from 2022’s leveraged buyout (LBO) activity allowing for a healthy and active leveraged financing environment.

- Dealers were net sellers of high yield bonds to the tune of $6.5 billion MTD and $7.8 billion YTD.

- Trading volumes were in line with the typical late summer holiday period averaging $6.6 billion a day over the last 20 days. Average high yield trading volumes are $10.2 billion MTD and $12.6 billion YTD.

- US Federal Reserve (Fed) policy meetings and subsequent rate decisions remain a key focus for credit markets as do economic indicators tied to inflationary trends and employment data. Recent data has indicated a softening in peripheral inflationary markers while the general economy continues to perform well.

Outlook

The US high yield market continues to defy investor expectations, many of whom came into 2023 expecting to see a more immediate downturn in the US economy.

Thus far, this narrative has not played out as expected and the US high yield market has responded positively to a US economy which continues to show signs of resilience. With headline inflation falling sharply, market expectations for a soft landing have increased progressively throughout the year. This has led the US high yield market to deliver a YTD performance to August 31st of +7.2%, outperforming higher quality fixed income asset classes such as US Investment Grade (+3.0%), US Treasuries (+0.6%) and short-term cash rates as proxied by the 0-3 month Treasury (+3.2%) (Source: ICE BofA).

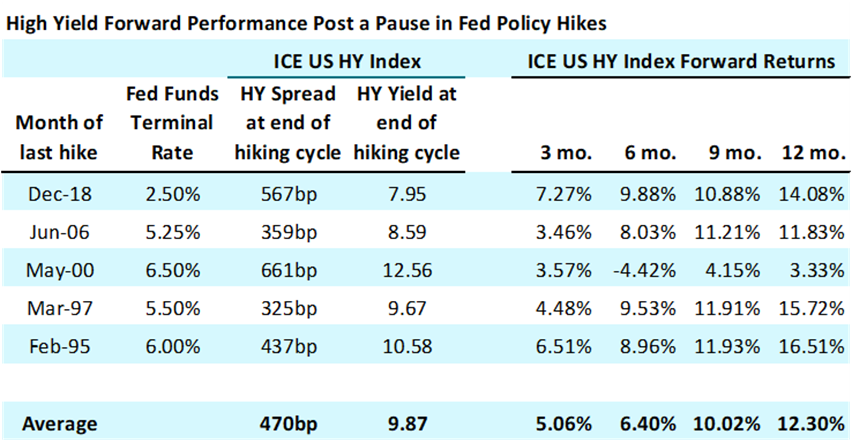

Although the Fed remains cautious as to how it signals where rates may go from here, we believe that we are at the end, or very close to the end, of the hiking cycle – after the most recent 25bps hike in July. This has typically been a very favourable entry point for high yield investors, as shown by the chart below – which highlights the average spread and yield across the previous five Fed hiking cycles, together with the forward-looking returns across various time periods:

Source: AXA IM, Bloomberg as of 31st August 2023

Although the market today appears a little expensive (mainly from a spread perspective) compared to average levels post a pause in Fed hikes, it would not take a lot for us to reach the average spread level of 470bps, which we hit as recently as May 2023. It is also worth noting that in two out of five of these hiking cycles, the spread at the end of the cycle was actually lower than today.

An important point to note is the forward returns after the last Fed hike, with an average 12-month forward return of 12.3%. The reason for this attractive level of return is, firstly, because the rise in interest rates corresponds to coupons being reset at higher levels and income taking over as a much more significant driver of returns. Secondly, the pass through of higher rates into the economy tends to drive a slowdown and sometimes outright recession, accompanied by an easing in Fed policy (i.e., rate cuts) which, although might see spreads widen in the short term, does not tend to last for long in typical credit cycles and may be positively offset through a lowering of underlying treasury yields.

Ultimately, whichever path the Fed takes, we expect GDP for the calendar years 2023 and 2024 to remain positive in the 0-2% range. This tends to mean the best of both worlds for the high yield market, in which many companies are able to deliver solid earnings growth, without suffering the effects of an economy which is running too hot and leads to increased costs for high yield companies through a combination of price inflation and higher interest expense via tightening monetary policy.

Annualised index performance

| 2022 | 2021 | 2020 | 2019 | 2018 | |

|---|---|---|---|---|---|

| ICE BofA US High Yield Master II | -11.2% | 5.36% | 6.15% | 14.41% | -2.24% |

Past performance is not a reliable indicator of future performance

References to companies and sector are for illustrative purposes only and should not be viewed as investment recommendations.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.