US outlook - Mild recession to see inflation fall

Key points

- The US economy appears to be heading for recession – we expect it to contract in the first half of 2023.

- Any recession looks set to be mild, though our GDP outlook of -0.2% and 0.9% for 2023 and 2024 is lower than consensus.

- The fall in output should loosen the labour market and alleviate inflation pressures. We forecast inflation to fall sharply albeit a little slower than consensus.

- Interest rates appear close to a peak – we estimate 5% – and are likely to remain at that level until 2024.

Recession or not?

The question facing the US is whether or not the economy will tip into recession. Our view since the summer has been that it will, and we now expect a recession starting in early 2023. Pinpointing dates is difficult, as recessions typically reflect the concerted reactions of consumer spending, hiring, investment and inventory – often influenced by external events. Recession in Europe, prompted by the energy shock as a result of the Ukraine crisis, will be a headwind to domestic activity – though we believe domestic dynamics will drive the US contraction.

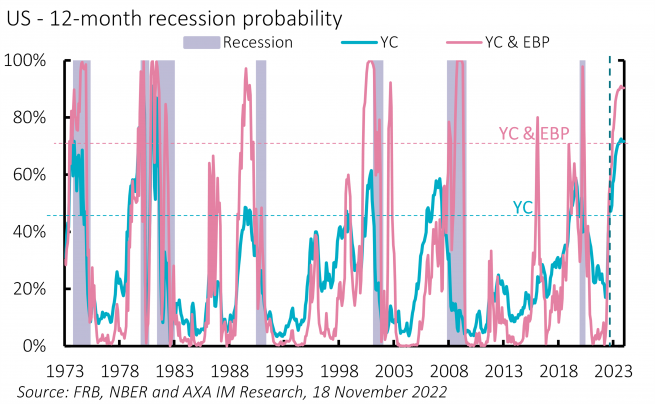

Our recession probability model suggests recession over the coming 12 months (Exhibit 4). As usual, this has preceded declines in survey evidence, for now simply suggesting deceleration. Two factors add to our conviction: First, inventory has risen sharply since the pandemic. The nature of GDP accounting – measuring the change in change of inventory – means that if inventory grows at a slower pace, as it is now doing, it weighs on activity. Recessions are typically driven by reversals in inventory. Second, downward revisions to the saving rate in the latest GDP release add to our view. These suggest households drew more heavily on savings to finance spending in 2022. This illustrates the strain on real incomes and suggests household buffers against future pressure are smaller.

For now, unemployment remains a subdued 3.7%, indicating the economy is not yet in recession. The Sahm rule – that observes that a 0.5 percentage point rise in unemployment over 12 months is a good indicator of recession – has not been met, though we forecast this for next year. We also see recession as consistent with the tightening in financial conditions, which has been sharper than the Federal Reserve (Fed) usually delivers in tightening phases – indeed, the sharpest since the 2001 and 2008 recessions.

A mild recession but growth below consensus

We forecast a mild recession, with a combination of weaker consumer spending, business investment and inventory adjustment resulting in GDP falling in Q1 to Q3 2023. Thereafter, we anticipate a return to growth but the expected sluggish fiscal and monetary policy responses are likely to drive only a modest pick-up, reflecting the end of the inventory adjustment, a recovery in real disposable income and firmer business investment.

The investment outlook will likely be critical. Corporate profit growth is likely to decelerate and fall outright throughout 2023 as energy, unit labour and finance costs rise and firms reduce profit margins. This is likely to lead to a fall in investment. However, energy investment should rise gradually – part of a global realignment of energy supply – which will help raise business investment by end-2023 and into 2024. Residential investment will also be important. This interest rate-sensitive category has reversed quickly from pandemic highs and is expected to still fall across 2023, though not as quickly.

We forecast GDP to fall from 1.9% in 2022 to -0.2% in 2023, including a mild recession, before rising to 0.9% for 2024. This is below the current consensus outlook of 1.8%, 0.4% and 1.4%.

We consider a number of upside risks. Energy could boost growth further, exceeding our cautious energy investment outlook, or contributing more through liquified natural gas exports. The labour market could continue to surprise in its resilience. We expect a small rise in unemployment to 4.5% by end-2023 but back to 4.2% by end-2024; more loosening may occur from falling vacancies than actual job losses. We assume a somewhat slower fall in inflation but if this occurs more in line with consensus, the boost to disposable income may be greater. The boost from pandemic savings may also be larger.

But there are also downside risks. We anticipate a relatively mild inventory correction compared to previous recessions, assuming recent supply chain issues create a higher demand for inventory, but a downturn may still force firms to scale back. Delayed policy stimulus could weigh more on the outlook, alongside the risk of a further tightening in financial conditions. We still envisage a modest rise in labour force participation, despite Congressional Budget Office projections to the contrary – overall, we consider the risks to be evenly balanced.

Inflation to fall but slower than markets forecast

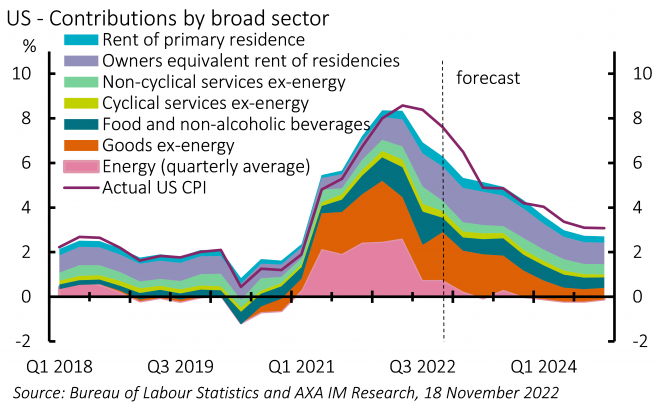

Inflation has been the biggest surprise this year. We forecast an average 8.2% for 2022 – double the rate we forecast a year ago. The Russian invasion of Ukraine accounted for much of that. However, unexpected labour market resilience has led to ongoing pressure in shelter and services inflation. With our outlook for a modest labour market correction, we forecast a slower fall in these components in the coming quarters.

We expect a sharp drop in inflation in 2023 and 2024, to average 5.1% in 2023 (4.2% in Q4 2023) and 3.4% in 2024 (3% by year-end) (Exhibit 5). However, consensus expectations are for inflation to average 4.2% next year and 2.4% in 2024.

Fed close to peak but far from cut

With higher inflation and a resilient labour market the Fed tightened aggressively this year. The Fed Funds Rate (FFR) stands at 3.75-4.00% at the time of writing, and as we had expected for some time, Fed Chair Jerome Powell has suggested it could moderate the pace of hikes from as soon as December. We also expect the Fed to tighten more slowly – by 25bps – in February and March next year. We forecast 4.75-5.00% as the peak but contend that labour market developments, rather than inflation, are likely to be critical. If the labour market remains tight, the Fed could tighten further, while a loosening could see a lower peak.

Our expectation of a slower fall in inflation makes us cautious of how soon the Fed will reverse policy. With core inflation expected well above target and a controlled labour market loosening, we expect the Fed to keep rates on hold at 5% throughout next year, against market expectations for a cut. We expect the Fed to begin cutting rates in 2024 and forecast an end of year rate of 3.75% (markets predict 3.50%). This would fall short of the 5% cuts seen during previous recessions (other than the pandemic). However, a mild recession, where unemployment looks set to remain relatively low and inflation still high, should warrant a more cautious easing in policy.

Caution also applies to the impact of the balance sheet. The Fed is conducting quantitative tightening (QT) at a far faster pace than before, but Powell suggested a minor impact – perhaps equivalent to a 25bp FFR hike per year. While highly uncertain, we think the QT impact has been exacerbated by the parallel large build-up of reverse repo holdings on the Fed’s balance sheet. The combination has squeezed excess reserves far faster than could have been anticipated. This may unwind next year. If it doesn’t, we expect the Fed to halt QT around mid-year, earlier than expected. If it does, a fast unwind could boost excess reserves and ease financial conditions further. Either could impact the outlook for rates.

Political outlook: From midterm to long term

As we write, the final midterm election results are still unknown. As expected, Republicans look likely to regain a majority in the House but by a small margin. As we suggested the Senate was tougher and Democrats have held the majority even before the last race in Georgia is decided on 6 December.

A divided government will mean policy gridlock, with no major bills likely to pass over the next two years. This could have an additional impact on a recession because, unlike Europe, the US relies on discretionary fiscal relief, rather than automatic fiscal stabilisers, to mitigate a slowdown. A divided government risks a slower and smaller stimulus. Tensions may also arise around spending bills and the extension of the debt ceiling.

The bigger impact may be on the 2024 Presidential Election. Donald Trump has announced he will stand for re-election but Trump-backed candidates did not fare well in the midterms, weakening his standing. President Joe Biden did better than his approval ratings suggested. As inflation falls with unemployment forecast around 4% by end-2024, the economy may work in his favour. But it is not obvious to us that the President will stand for a second term, which could mean two new candidates for 2024.

Our views for 2023

Read our full outlook to find out more about our experts' views.

Read our regional outlooks

Eurozone outlook - Difficult roads ahead

China outlook – A bumpy path to reopening

UK outlook – Navigating troubled waters

Japan outlook – Recovery appears set to continue

Emerging markets outlook – Darkest before dawn

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, BNP Paribas Asset Management, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2026 BNP Paribas Asset Management. All rights reserved.